Why Tampa Bay Is Now a Foreclosure Hotspot in 2025

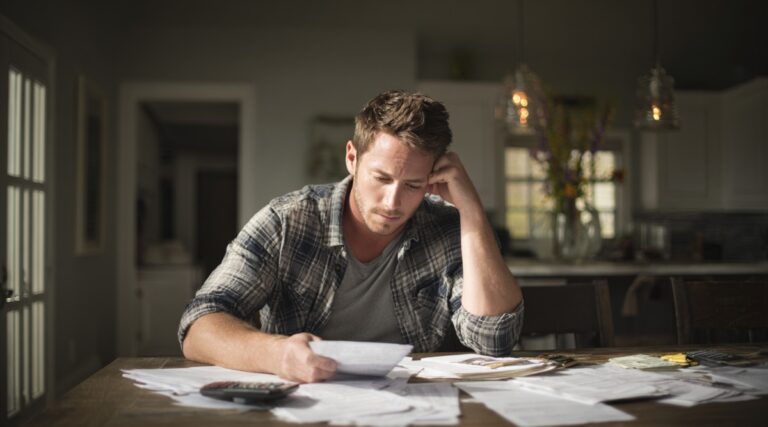

Tampa Bay has recently become one of the fastest-growing foreclosure markets in the country. Reports show that the region is now leading the nation in new foreclosure filings, placing thousands of homeowners at risk. Rising interest rates, insurance increases, and post-pandemic financial strain have created a perfect storm that is putting families under pressure.

But even with these trends, homeowners in Tampa Bay have rights — and most residents are unaware of the protections available to them under Florida law. Understanding how foreclosures begin, how lenders operate, and how to respond early can often change the outcome completely.

The Hidden Factors Driving Foreclosures in Our Region

Several forces are pushing foreclosure numbers higher than the national average. The most common include:

1. Significant Home Insurance Premium Increases

Insurance costs have soared across Florida, with Tampa Bay experiencing some of the steepest jumps. Many homeowners are facing yearly increases of 30–80%. When insurance is escrowed into the mortgage, even a moderate premium increase can raise monthly payments beyond what a family can manage.

2. Adjustable-Rate Mortgages Resetting at Higher Rates

Many homeowners who purchased homes during the low-rate years did so with ARM loans. As rates shift upward, monthly payments climb sharply, creating unexpected financial hardship.

3. Post-Pandemic Hardship and Expired Forbearances

The final wave of COVID-19 forbearance programs has ended. Homeowners who were covered by temporary payment plans are now facing large catch-up balances or recalculated monthly payments that are no longer affordable.

4. Mortgage Servicing Errors and Miscommunication

Mistakes by mortgage companies are more common than most homeowners realize. Misapplied payments, incorrect escrow calculations, and inconsistent communication can all contribute to default notices — even when the homeowner is doing everything they can to stay on track.

If you are experiencing any of these issues, the problem may not be your fault. Our Foreclosure Defense page explains how these errors can impact your rights and what legal options may be available.

The Early Warning Signs That a Foreclosure May Be Coming

Foreclosures almost never begin overnight. Most families experience months of confusion, mixed messages, or unclear notices before the process becomes official. Common red flags include:

- Mortgage statements that suddenly increase without explanation

- Letters stating your loan is “in default” or “past due” when you disagree

- Repeated phone calls from your mortgage servicer pressed as “urgent”

- Conflicting information between mailed letters and what the servicer says by phone

- Notices that your mortgage has been transferred to a new company

- Payments being rejected or returned

- Escrow shortages that weren’t disclosed earlier

If you have received any of the above, do not ignore them. Early action often leads to better solutions.

The Common Mistakes Homeowners Make When Foreclosure Looms

When stress is high, emotions take the lead — and homeowners sometimes make choices that unintentionally harm their case. These are the errors we see most often:

Waiting Too Long to Get Legal Help

Many homeowners hope the problem will fix itself or assume the lender will work with them. Unfortunately, this allows the foreclosure timeline to continue moving forward.

Relying on Verbal Promises From Servicers

Mortgage companies often say one thing on the phone but send conflicting written notices. Only the written notices matter legally.

Failing to Document Communication

Every letter, every call, every message counts. Documentation can be used as evidence if the lender violates your rights.

Submitting Applications Without Legal Review

Loss mitigation forms, hardship letters, and supporting documents must be filled out accurately. Even small errors can stall or derail your application.

For guidance on avoiding these traps, review our page on COVID Debt Protection, which explains how hardship-related cases are handled in Florida.

Your Rights Under Florida Foreclosure Law

Florida is a judicial foreclosure state, which means lenders must go through the courts before they can take your home. That gives homeowners meaningful rights, including:

- The right to challenge inaccurate mortgage balances

- The right to request a full payment history and accounting

- The right to dispute improper fees or charges

- The right to legal representation in court

- The right to stop foreclosure if the lender made certain procedural mistakes

Florida law also restricts what lenders can do while a loss mitigation application is under review. To learn more, see our detailed breakdown on dual tracking issues.

How We Help Tampa Bay Homeowners Protect Their Homes

Rebbecca Goodall Law works with homeowners at every stage of the foreclosure process — from the first late notice to active litigation. Our approach is both legal and strategic. We help clients by:

- Reviewing loan histories for errors

- Identifying violations that pause or challenge foreclosure actions

- Negotiating repayment or modification solutions

- Holding lenders accountable for mishandled applications

- Defending homeowners directly in court when necessary

If your home is in danger, our Foreclosure Defense page outlines the protections available under state and federal law.

What You Should Do If You’re Worried About Losing Your Home

If foreclosure seems possible, take these steps immediately:

- Save every letter and notice from your mortgage company

- Request a complete payment history

- Write down dates and times of all servicer calls

- Keep copies of all payments or attempted payments

- Speak with a foreclosure defense attorney as early as possible

You do not have to navigate this alone. Many families in Tampa Bay are facing the same challenges — and with the right help, the outcome can look very different.

Rebbecca Goodall Law fights to protect homeowners across Elfers, New Port Richey, Holiday, Tarpon Springs, Beacon Square, and surrounding areas.

If you’re unsure whether your lender is acting lawfully, contact us. One conversation can change every next step.